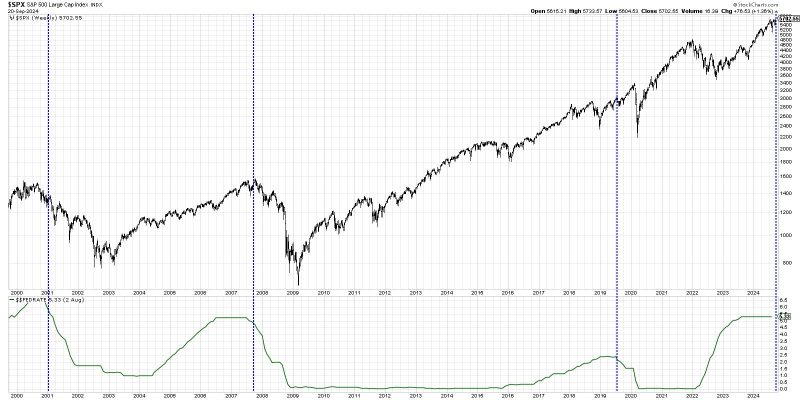

When it comes to their effect on stock performance, interest rate cuts often appear as a double-edged sword. On one side, these cuts seem to stimulate economic activity and theoretically could cause bulls to charge. Alternatively, rate cuts can be interpreted as reactions to a faltering economy, a sign which grizzly bears may find appealing. The following discourse will attempt to decode the correlation between rate cuts and stock performance, revealing the truth hidden beneath the surface.

At a foundational level, interest rate cuts are used by central banks as tools for promoting economic growth. When entities such as the Federal Reserve decrease interest rates, borrowing costs for companies and individuals decline. This outcome can, in turn, promote spending and stimulate wider economic activity. Companies may find it easier to finance expansionary efforts and consumers could feel more comfortable making purchases, both of which result in increased revenues for businesses.

To investors and stock traders, these processes paint a very bullish picture. Businesses expanding their operations and generating additional revenues can be interpreted as growth prospects for those companies, enticing investors to buy their stocks. The increased demand for these stocks then drives up prices, leading to a bullish trend in the stock market.

However, the same rate cuts often have a more ominous interpretation, justifying a bearish outlook on stocks. Typically, central banks implement rate cuts as a response to an already weakening economy. High inflation rates, decreasing job opportunities, declining GDP; these are all signs of economic strife which could cause central banks to slice the interest rates.

Stock traders with a bearish predisposition emphasize this aspect of rate cuts. The reality is that despite the initial uplift from lower borrowing costs, the underlying softness of the economy could have far-reaching implications for the profitability of companies. If consumer confidence drops and unemployment rates spike, demand for products and services may wane, negatively affecting revenues and therefore, the companies’ stock performances.

Furthermore, while lower interest rates make funding cheaper for companies, they also decrease the earnings from cash reserves that the businesses have parked in banks. This can be especially impactful for financial institutions such as banks, whose profit margins can be significantly decreased due to this lower interest income. Hence, a bearish trend may show itself in the stock market post-rate cuts.

The link between rate cuts and stock performance is thus highly contingent on the lens of perception. Bulls will see an opportunity for growth, even in a gloomy economic environment, spurred by potentially fruitful effects of lower borrowing costs for businesses and consumers. On the other hand, bears will focus on the root cause of rate cuts – a weakening economy – and its subsequent impacts on company revenues and profitability.

In this context, contrary to the adage, ‘one size fits all,’ economic circumstances and individual perceptions play crucial roles in discerning how rate cuts influence stock performances. Investors need to thoroughly evaluate the state of the economy, the justifications for the rate cuts, and the likely behavioral response of both companies and consumers. Whether one turns out to be bullish or bearish in the face of rate cuts is largely dictated by these factors.

Mitigating the debate between bullish and bearish outlooks, it seems clear that the relationship between interest rate cuts and stock performance is complex. The nature of rate cuts as both economic stimuli and indicators of economic distress make them inherently ambiguous in terms of their longer-term effects on stocks. Thus, it behooves investors to approach this subject carefully, conducting thorough research and maintaining a balanced perspective, before formulating their investment strategies.